COLOMBO, March 10, 2026

The chairman of Sri Lanka’s state-run Ceylon Petroleum Corporation (CPC), D.A. Rajakaruna, appeared before the media on March 10 to defend a sharp retail fuel price increase that took effect the same day. The explanation he offered centred on two claims: that global oil prices had risen “nearly 100 percent between the 1st and the 27th” of February into early March, and that a domestic panic-buying surge had drained reserves far sooner than anticipated.

Both claims contain elements of truth. Both also require substantial qualification.

What the CPC Chairman Said

Rajakaruna stated that between March 1 and March 9, Sri Lanka consumed 59,200 metric tons of diesel and 47,500 metric tons of 92-octane petrol — volumes he said had been expected to last until mid-month. He attributed the accelerated drawdown to public anxiety over potential shortages, and said the lower-cost stocks procured before the price spike had therefore been exhausted earlier than CPC modelled.

He repeatedly urged the public not to panic-buy and stressed that the price adjustment was unavoidable given the external cost environment.

The Price Claim: What Market Data Show

The central evidentiary problem with the CPC chairman’s account is the “near-100 percent” figure for global oil price increases.

Brent crude — the international benchmark against which Sri Lanka’s import contracts are priced — closed February 2026 in the low $70s per barrel. According to Reuters commodity data and the U.S. Energy Information Administration’s weekly petroleum report, Brent stood at approximately $71.32 per barrel on February 27, having risen from a January monthly average of roughly $66.60. That represents a month-on-month increase of approximately 7 percent.

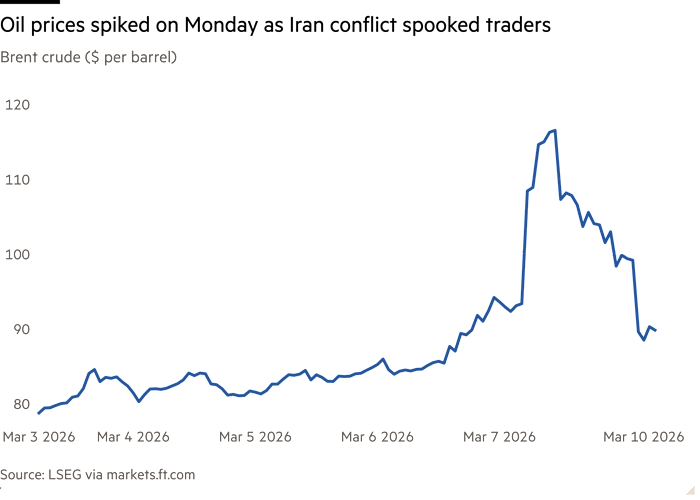

In early March, a sharp but short-lived spike occurred. Geopolitical tensions linked to U.S. and Israeli military actions against Iran drove Brent to intraday highs near $119–$120 per barrel around March 7–9 — a peak of roughly 55–60 percent above early-March levels near $77, according to Reuters and ICE Futures Europe trading data. That spike, at its maximum, does not reach the “near-doubling” threshold cited by Rajakaruna.

Critically, by March 10 — the date of the price hike — Brent had retreated sharply. Closing prices on that date were recorded in the range of $82.60 to $88 per barrel across major exchanges (Reuters, CME Group), representing a single-day decline of more than 10 percent from the spike’s peak. The market was moving against the emergency narrative at the very moment the narrative was being deployed.

J.P. Morgan and UBS, in research notes published this month, noted that while the Iran-linked tensions created a temporary premium, underlying supply fundamentals pointed to average 2026 Brent prices in the $60–$72 range absent a sustained disruption. As of March 10, no sustained disruption had materialised.

The Consumption Claim: Elevated, But Context Matters

The reported consumption volumes — approximately 6,578 metric tons of diesel per day and 5,278 metric tons of petrol per day over the nine-day period — do indicate elevated demand relative to historical norms.

Sri Lanka’s annual fuel consumption averages around 110,000–115,000 barrels per day across all fuels, according to the Ministry of Power and Energy’s 2024 annual statistical digest. Diesel typically accounts for approximately 38,000–40,000 barrels per day (roughly 5,000–5,500 metric tons), with petrol at approximately 28,000–29,000 barrels per day (3,500–4,000 metric tons). The nine-day figures therefore represent an increase of roughly 30–60 percent above normal daily consumption for each fuel.

The consumption surge is, in other words, real. The question is whether it justifies the pricing response characterised as externally inevitable, or whether it reflects a policy decision the CPC was going to make in any case.

The Reassurance Problem

What complicates the CPC’s account further is the timeline of its own public communications.

As recently as March 2–3, CPC officials — including Rajakaruna — told journalists and issued public statements assuring adequate fuel stock: petrol for 37 days, diesel for 35 days, with confirmed shipments through the end of March and into April. On March 2, a public holiday, the corporation distributed more than five million litres of fuel to meet demand, while publicly maintaining that no shortage risk existed.

A price increase implemented on March 10 — within a week of those assurances — demands a more explicit accounting of what changed, and when. The CPC has not provided a day-by-day consumption log, import invoice data, or a formal revised stock position as of the date of the increase. Without that, the public and the market are being asked to accept a narrative of external inevitability on the basis of a chairman’s media appearance alone.

Two Separate Questions

It is important to distinguish between two distinct claims, which the CPC’s account conflates.

The first is whether the price increase was justified on cost grounds. Sri Lanka prices fuel on a cost-reflective basis, and genuine import cost increases would warrant adjustment. If CPC’s March purchase contracts were locked in at or near the $119 spike price, that would be materially relevant — but those contract details have not been disclosed.

The second is whether the specific characterisation — a near-doubling of global prices — is accurate. On this question, the answer from the data is clearly no. Brent did not double in February or early March. It spiked sharply and briefly, and had already retreated significantly by March 10.

The Broader Stakes

Sri Lanka’s public trust in state energy institutions remains fragile after the 2022 economic crisis, when fuel shortages paralysed the country for months and contributed directly to the political upheaval that followed. CPC’s credibility is not a minor institutional asset; it is load-bearing infrastructure for the government’s economic recovery narrative.

As Middle East tensions persist — with the Iranian situation unresolved as of this writing — further volatility in global oil markets cannot be ruled out. Transparent, evidence-based communication about the pricing mechanism and stock positions is not only a matter of public interest. At this stage, it is a matter of national economic management.